USDT remains the market’s liquidity anchor

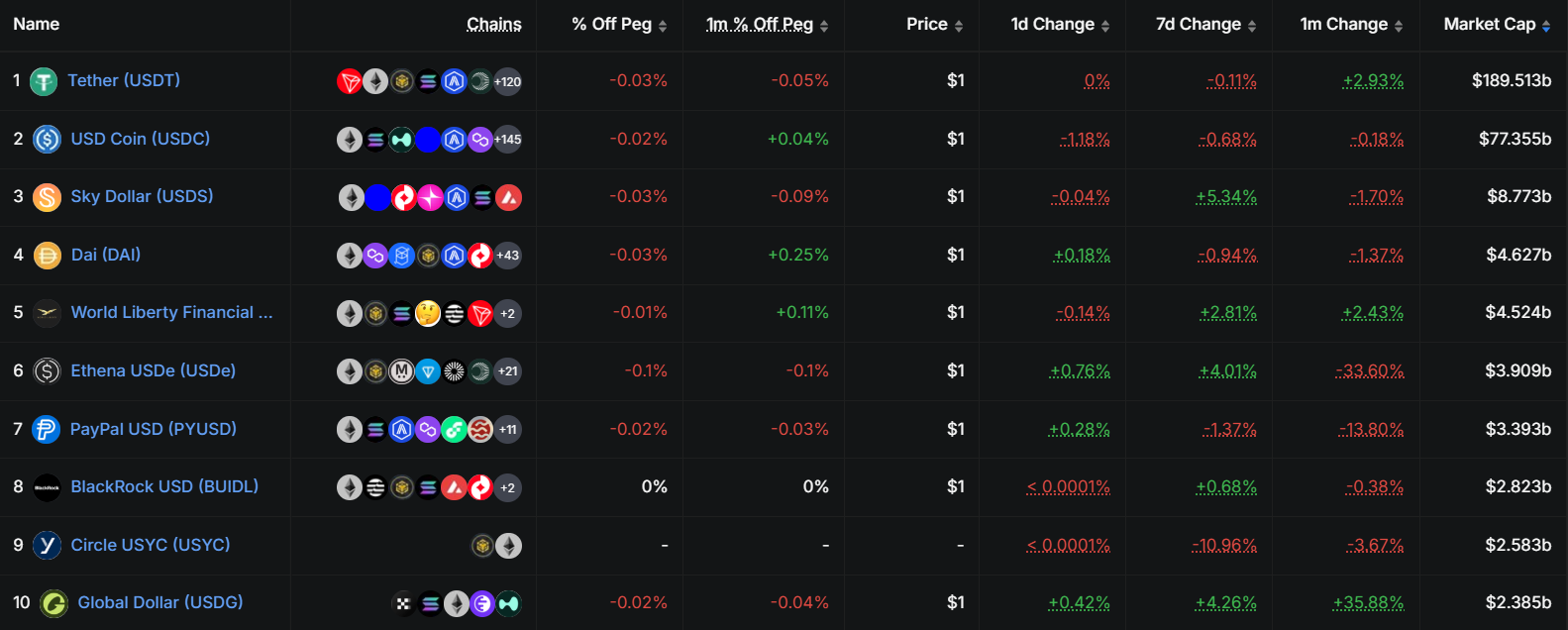

USDT remains the largest stablecoin by market cap, holding around $189.507 billion. USDC follows at around $77.351 billion, while USDS, DAI, and USD1 remain much smaller at around $8.773 billion, $4.627 billion, and $4.527 billion, respectively.

Top 5 stablecoins by market cap from DeFiLlama, as of May 4 2026.

That gap keeps Tether well ahead of every other issuer by circulating supply. It also gives USDT a clear advantage across exchange liquidity, trading pairs, cross-border settlement, and crypto-native dollar demand.

USDT is still the default liquidity layer for much of the digital asset market. Market participants often do not choose USDT because it is the newest or most regulated option. They choose it because it is available, liquid, widely supported, and deeply embedded across trading venues.

Why USDT still leads

USDT’s lead is built on distribution. It is accepted across centralized exchanges, decentralized finance (DeFi) protocols, payment corridors, peer-to-peer markets, and treasury workflows. That network effect is difficult to displace.

Its core advantages remain clear:

-

Liquidity depth: USDT remains one of the most widely traded dollar-denominated assets in crypto.

-

Exchange coverage: It is deeply integrated across spot, futures, and settlement pairs.

-

Emerging-market utility: USDT is often used where access to dollar banking is limited or costly.

-

Operational familiarity: Many market participants already treat USDT as the standard trading unit.

This gives Tether a scale advantage that newer stablecoins cannot easily replicate. A competitor can offer stronger regulatory positioning or cleaner institutional branding, but liquidity habits tend to change slowly.

Transaction volume confirms USDT’s network effect

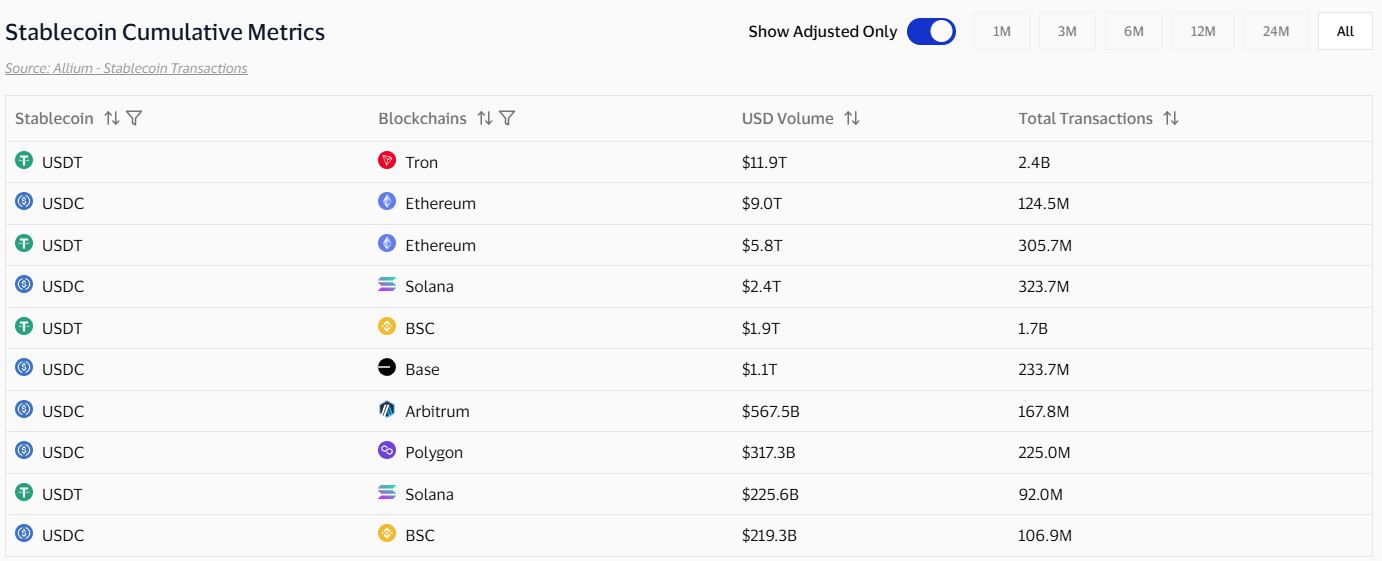

USDT’s market cap lead is backed by heavy transaction activity. On Tron, USDT has processed around $11.9 trillion in volume across 2.4 billion transactions. On Ethereum, USDT has handled around $5.8 trillion in volume across 305.7 million transactions.

Stablecoin cumulative metrics from Visa, as of May 4, 2026.

Those figures explain why USDT remains difficult to displace. Its lead is not only based on exchange listings or supply. It is also supported by real transaction activity across high-volume networks.

The clearest takeaway is that USDT’s dominance is strongest where stablecoins are used as working capital: transfers, exchange settlement, cross-border movement, and crypto-native liquidity routing.

Tron remains central to USDT’s scale

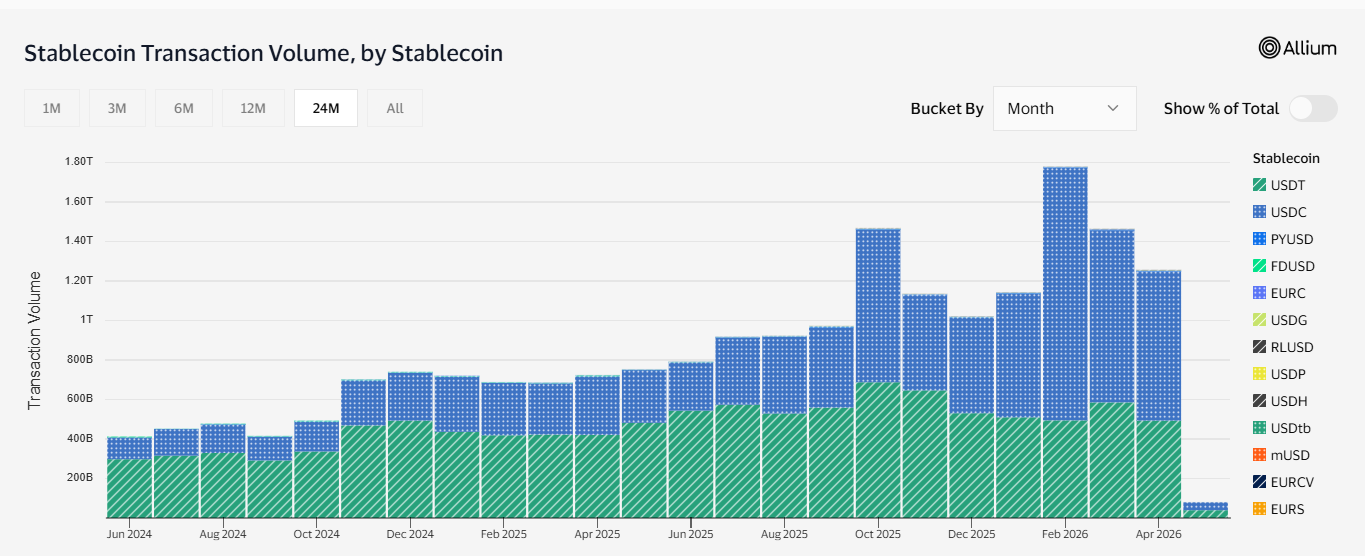

USDT’s strongest transaction footprint comes from Tron. That is important because Tron has become one of the main networks for stablecoin transfers, especially where speed, low fees, and broad wallet support matter.

Stablecoin transaction volume by stablecoin from Visa, as of May 2026.

This gives USDT a practical advantage. Market participants often choose the rail that is cheapest, fastest, and most accepted. Tron-based USDT fits that role across many retail and peer-to-peer corridors.

USDC has stronger institutional positioning in several markets, but USDT’s Tron activity shows why practical liquidity still matters. Stablecoin dominance is not decided only in regulated finance. It is also decided in daily settlement behavior.

Fiat-backed stablecoins still dominate the sector

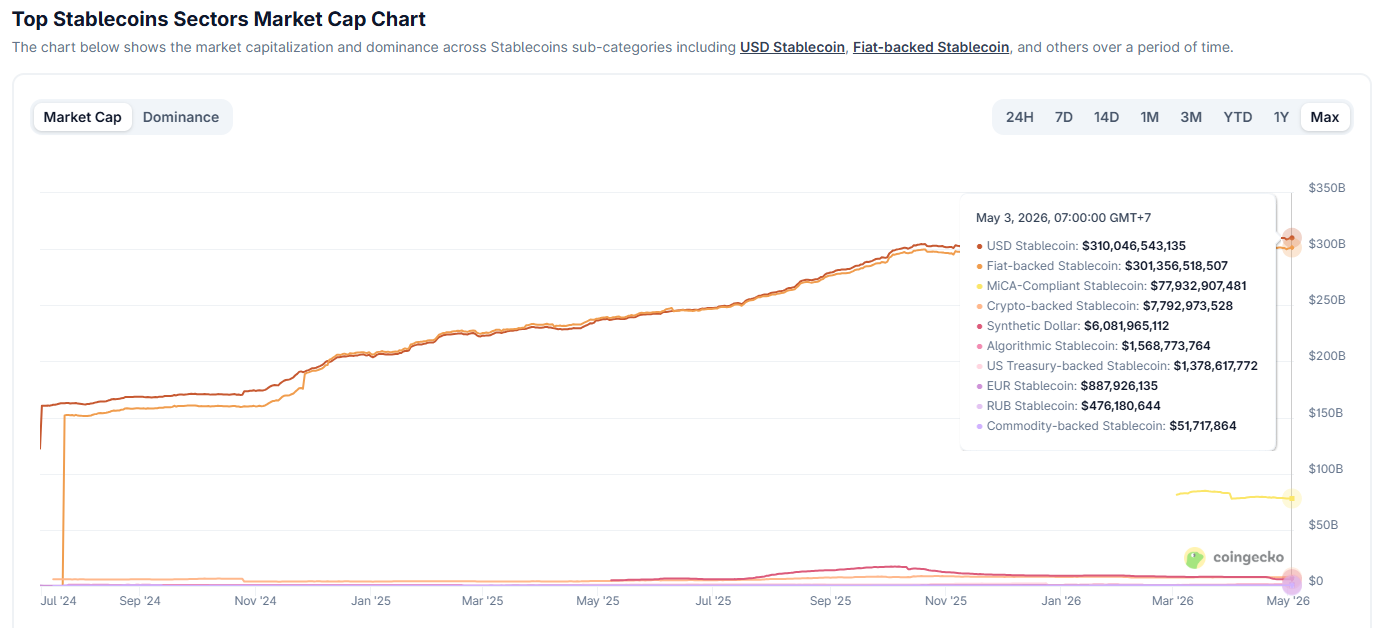

Stablecoin growth remains concentrated in fiat-backed assets. The fiat-backed stablecoin category stands at around $310.648 billion, far ahead of crypto-backed stablecoins, algorithmic stablecoins, and commodity-backed stablecoins.

Top stablecoin sectors market cap chart from CoinGecko, as of May 4, 2026.

This supports USDT’s leadership. The market still prefers stablecoins that provide a direct dollar reference, broad exchange support, and simple settlement utility. More specialized stablecoins may keep growing, but fiat-backed assets continue to define the sector’s core structure.

Reserve strength is still central to the debate

Tether’s reserve structure remains a key reason USDT stays relevant and a key reason it remains scrutinized.

USDT reserves are predominantly held in U.S. Treasury bills, worth around $117 billion as of end-March 2026. Gold represented about 10% of USDT reserves, while Bitcoin accounted for around $7 billion.

This reserve mix supports Tether’s profitability and liquidity profile, but it also keeps attention on asset composition. Short-dated U.S. government debt is generally viewed as high-quality collateral. Gold and Bitcoin add diversification, but they also make the reserve discussion more complex than a simple cash-and-Treasury model.

For USDT, the reserve question is not only about backing. It is also about confidence. The larger USDT becomes, the more its reserve strategy affects how institutions, regulators, and exchanges assess systemic exposure.

USDC is growing, but it still trails USDT

Circle’s USD Coin (USDC) remains the clearest challenger. Its strength comes from regulatory positioning, institutional partnerships, and deeper alignment with U.S. payment infrastructure.

USDC circulation rose 72% year over year to $75.3 billion in the fourth quarter, supported by stronger stablecoin adoption and favorable regulation in the United States. Circle also received conditional approval for a national trust bank charter and formed partnerships with Visa and Polymarket.

That growth is meaningful, but it does not erase the gap. USDC has stronger institutional optics in several markets, while USDT still has a larger trading footprint and broader global usage base.

The market is now split across 2 leadership lanes:

-

USDT: Liquidity, exchange depth, global transfers, and crypto-native settlement

-

USDC: Regulated U.S. positioning, institutional access, payment partnerships, and compliant on-chain finance

Both can grow at the same time. USDC does not need to replace USDT to become more important. It only needs to keep expanding across regulated settlement, enterprise payments, and institution-facing channels.

Stablecoins are becoming financial infrastructure

Stablecoins are no longer just trading tools. They now sit closer to payment infrastructure, treasury management, settlement, and dollar access.

Stablecoin market capitalization rose above $300 billion in early 2026, while transaction volume climbed 72% in 2025 to around $33 trillion. This growth points to a demand layer tied to real payments and settlement activity, not only speculative trading.

Stablecoin market cap from Coinglass, as of May 2026.

Stablecoins were originally designed to support crypto exchange trading, but they have moved toward broader use cases, including cross-border payments and tokenized financial services. That shift raises the standard for stablecoin issuers, especially around reserve quality, redemption reliability, compliance systems, and issuer transparency.

USDT benefits from scale. USDC benefits from regulatory clarity. New entrants may benefit from specialized use cases, bank partnerships, ecosystem incentives, or tokenized asset integrations.

What could weaken USDT’s lead?

USDT’s leadership looks secure today, but it is not risk-free.

The main pressure points are:

-

Regulatory divergence: Tighter rules in the U.S., Europe, or major Asian markets could favor issuers with stronger local licensing.

-

Institutional preference: Banks, asset managers, and payment companies may prefer stablecoins with clearer legal structures.

-

Reserve scrutiny: Any concern over asset quality, redemption capacity, or disclosure standards could affect confidence.

-

Specialized competition: USDC, USD1, and bank-linked stablecoins could gain share in enterprise, ecosystem-specific, and regulated settlement channels.

These risks do not automatically threaten USDT’s dominant position. They define where competition is most likely to intensify.

USDT still leads in the market that exists today. The next phase may reward stablecoins that combine liquidity, compliance, transparency, and payment infrastructure in one package.

The bottom line

USDT still leads the stablecoin market. Its dominance is backed by liquidity, distribution, exchange integration, and global dollar demand. Its market cap remains far ahead of USDC, and its transaction footprint across Tron and Ethereum shows deep usage across major stablecoin rails.

The more important shift is structural. USDT remains the market’s liquidity leader, but stablecoin competition is moving beyond market cap. The next phase will be shaped by regulation, institutional adoption, reserve design, and payment utility.

USDT is still the leader. The stablecoin market is now large enough that leadership will be judged by more than size.

This article is for informational purposes only and does not constitute financial advice. Always do your own research (DYOR) before making any decisions.

Trade stablecoins and crypto markets on Toobit

USDT remains one of the most important settlement assets in crypto, especially for market participants tracking liquidity, market rotation, and dollar-denominated pairs.

Toobit gives market participants access to spot and futures markets with the tools needed to follow stablecoin liquidity and trade major crypto assets in real time.

Start trading on Toobit today.