TradFi runs on institutions and regulated rails. DeFi runs on wallets and smart contracts, always on.

Source: Toobit

Traditional finance (TradFi) and decentralized finance (DeFi) are two parallel systems shaping how people save, borrow, invest, and make payments.

TradFi is the established, regulated stack built around banks and capital markets. DeFi is the newer, blockchain-based stack that uses smart contracts to run financial services on public networks.

This guide gives you a clear comparison of how TradFi vs. DeFi works, where each shines, and what to watch out for.

What is TradFi and DeFi?

Before we get into the spicy part (differences), here are some quick definitions of what each term is and how they work.

What is TradFi?

TradFi is the conventional financial system of banks, brokers, stock and bond markets, insurers, and payment networks governed by laws and regulators such as the Federal Reserve, the U.S. Securities and Exchange Commission (SEC), and the Financial Conduct Authority (FCA) in the U.K..

How TradFi works in real life

-

Institutions custody funds: Your money typically sits in accounts controlled by banks or brokerages.

-

Identity is required: Most services run on Know-Your-Customer (KYC) or anti-money laundering (AML) checks and documentation, because regulators demand it.

-

Transactions settle on financial rails: Card networks, automated clearing houses (ACHs), wire systems, and market infrastructure move money and securities with rules, cutoffs, and settlement windows.

-

Protections exist (with limits): In the U.S., Federal Deposit Insurance Corporation (FDIC) deposit insurance covers up to $250,000 per depositor, per FDIC-insured bank, per ownership category.

TradFi is slow to change for a reason. When the stakes are salaries, mortgages, pensions, and national payment systems, speed comes second to stability.

What is DeFi?

DeFi refers to financial services built on public blockchains (like Ethereum and various Layer 2 networks) using smart contracts instead of banks or brokers. DeFi is usually crypto-native and often permissionless, meaning anyone with a wallet and internet access can participate.

How DeFi works in real life

-

You custody your assets: Most DeFi is non-custodial. Your wallet, your keys, your responsibility.

-

Smart contracts run the rules: Code defines how swaps, loans, collateral, and liquidations work, and executes automatically on-chain.

-

Transparency is default: Transactions and reserves can be inspected on public ledgers and dashboards (total value locked [TVL] is commonly tracked via tools like DeFiLlama).

-

Always-on markets: DeFi runs 24/7 with settlement often measured in seconds or minutes, depending on the network.

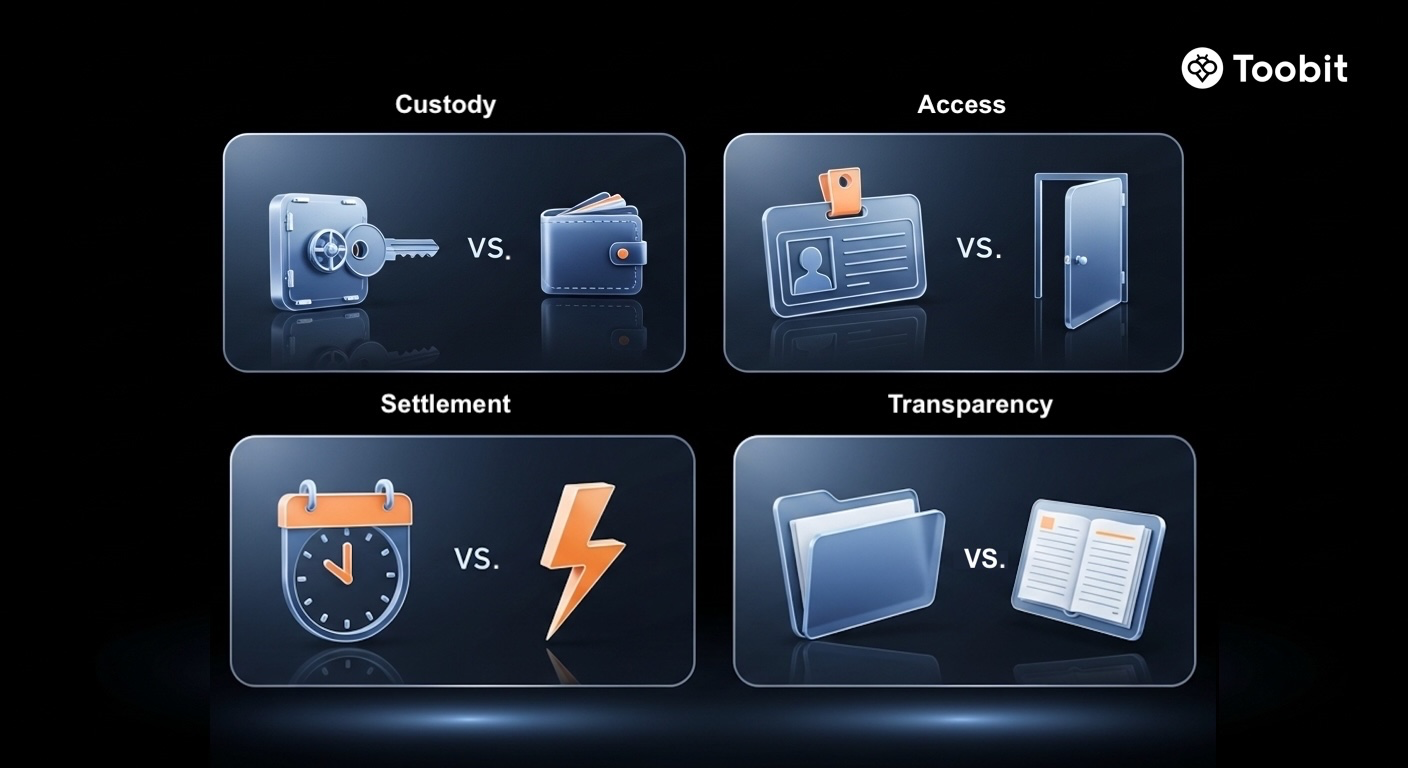

What are the differences between TradFi and Defi?

Both systems provide financial services, but they diverge across control, access, transparency, technology, and risk.

A quick scan of the big TradFi vs DeFi differences: custody, access, settlement speed, and transparency.

Source: Toobit

Here is a table comparing the differences between TradFi and DeFi across 8 different factors.

|

Comparison factor |

TradFi |

DeFi |

|

Control and custody |

Banks and brokers custody assets and can freeze or reverse activity under policy or legal orders. |

Users self-custody assets via wallets and control access using private keys. |

|

Intermediaries vs. smart contracts |

Institutions, compliance teams, and legal agreements enforce rules. |

Smart contracts automate rules, from interest rates to liquidations, with minimal human intervention. |

|

Permission and access |

Requires identity checks and often credit checks. Access can be limited by geography, documentation or banking coverage. |

Typically open to anyone with a compatible wallet, enabling broader access without traditional account opening. |

|

Regulation and protections |

Heavily regulated with consumer protections (deposit insurance, disclosure rules, licensing). |

Regulations are evolving; formal protections are limited and vary by jurisdiction. |

|

Transparency |

Disclosures exist, but most balance sheet risk is not visible in real time. |

On-chain activity is publicly auditable by default (with the trade off that users must verify it themselves). |

|

Settlement and operating hours |

Market hours and settlement cycles still apply in many venues. |

24/7 execution with fast settlement, subject to network conditions. |

|

Fees |

Fees can be layered (spreads, account fees, intermediaries, cross-border charges). |

Fees are commonly gas fees plus protocol fees, which can be low on some networks but can spike during congestion. |

|

Identity model |

Real-name identity tied to documentation and credit history. |

Wallet-based identity is typically pseudonymous by default (privacy upside, fraud downside). |

Are TradFi and DeFi similar in any way?

Yes. Strip away the tech and branding, and both systems chase the same core jobs:

-

Payments, savings, lending, borrowing, trading, and hedging: Same financial verbs, different plumbing.

-

Markets and price discovery: Supply and demand still run the show, whether it is an exchange order book or an automated market maker (AMM) pool.

-

Risk management exists in both: Collateral, diversification, and leverage appear everywhere. The mechanics differ, but the intent is familiar.

-

Boom-bust cycles happen: TradFi has had systemic crises (2008). DeFi has had liquidation cascades and stress events tied to volatility.

They are also becoming more interconnected through tokenized assets, stablecoin settlement, and experiments that blend regulated rails with on-chain execution.

For example, JPMorgan's Kinexys (formerly Onyx) now processes over $2 billion daily for interbank settlements. Simultaneously, BlackRock's BUIDL fund has surpassed $1.7 billion in assets on Ethereum, and the repeal of SAB 121 in 2025 has finally allowed major U.S. banks to provide digital asset custody at scale.

There has also been a rise in "Internet Bonds" like Ethena (USDe). By early 2026, USDe peaked at over $10 billion in TVL, using a delta-neutral strategy to create a synthetic dollar. It acts like a DeFi-native version of a high-yield savings product, providing a benchmark "risk-free" rate for the on-chain economy without relying on traditional bank collateral.

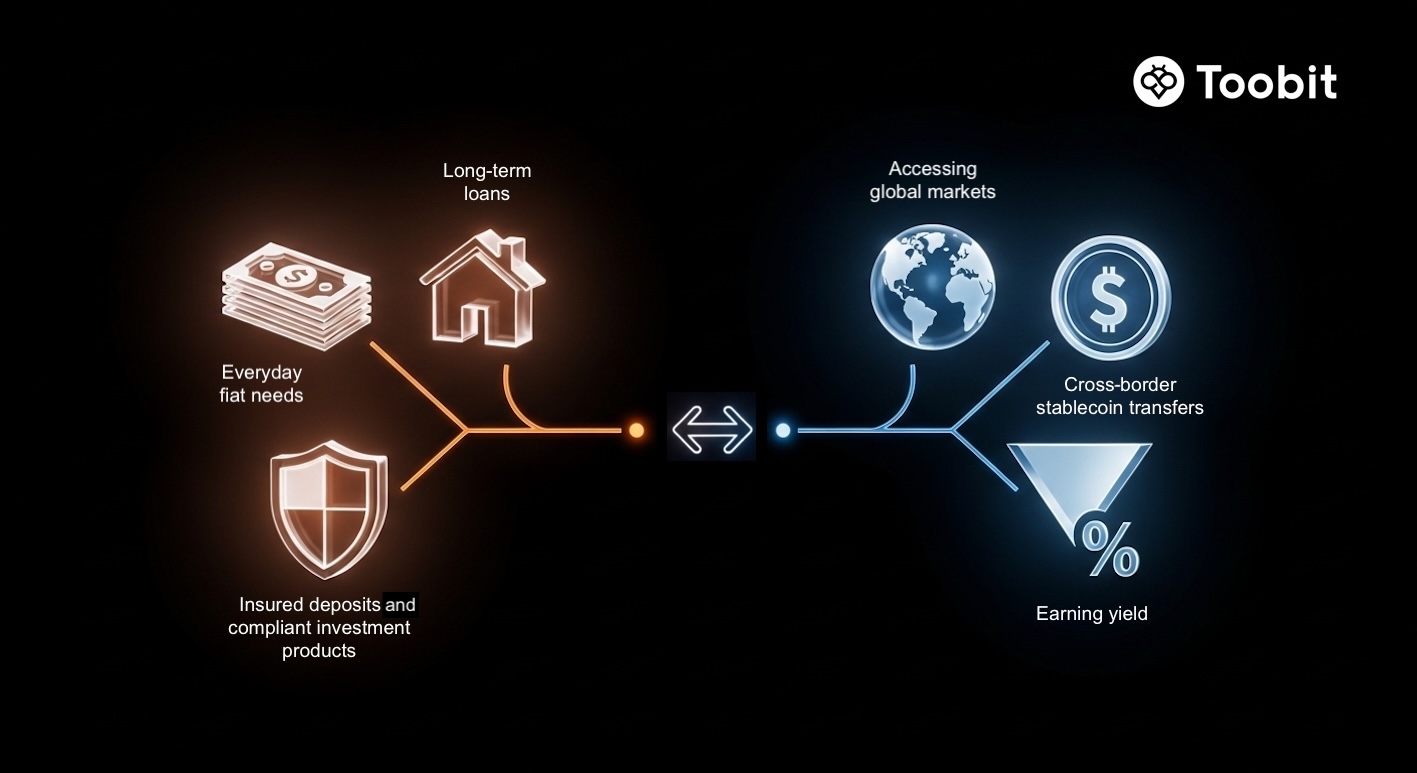

When to Use TradFi vs. When to Use DeFi

Most people do not need a religious war here. The smarter move is usually match-the-tool-to-the-job.

Use TradFi for regulated essentials. Use DeFi for on-chain speed and flexibility, if you can manage the risks.

Source: Toobit

TradFi is generally more appropriate for:

-

Salaries, taxes, and everyday fiat needs

-

Long-term loans (mortgages) with legal enforcement

-

Insured deposits and regulated consumer protection (for funds you cannot afford to lose)

-

Large corporate financing and compliant investment products

DeFi can be advantageous for:

-

Accessing global markets when local banking is limited

-

Fast, cross-border transfers using stablecoins

-

Earning yield on crypto holdings (with clear risk acceptance)

-

Trying financial products that move faster than traditional product cycles

Hybrid approach

A common playbook is to keep the essentials in TradFi for stability and protection, while using DeFi with a defined allocation and strict security hygiene.

Risks and limitations of each system

Both systems have risks. They just fail differently.

Different systems, different failure modes. Know the risks before you commit capital.

Source: Toobit

TradFi limitations

-

Access barriers: Documentation, minimum balances, and credit history can exclude people; the World Bank's Global Findex 2025 report estimated 1.3 billion unbanked adults in 2025.

-

Concentration and systemic risk: Large institutions can create cascading failures under stress.

-

Limited real-time transparency: Users usually cannot inspect bank risk exposures day to day.

-

Operational constraints: Cutoffs, business hours, and cross-border friction still exist.

DeFi risks

-

Smart contract exploits: Hacks remain a major risk. Chainalysis and Reuters have cited $3.8 billion stolen in 2022 across crypto hacks, with DeFi frequently a major target.

As of 2026, protocols like Nexus Mutual have become a standard requirement for "Institutional DeFi" users. This layer of decentralized protection provides a safety net against code vulnerabilities, helping to mitigate the "unrecoverable" nature of early DeFi hacks.

-

Volatility and liquidation cascades: Collateral values can drop fast, triggering automated liquidations.

-

Regulatory uncertainty: Rules vary and continue to change.

-

User-side security: Key loss, phishing, and malicious approvals can be unrecoverable.

Neither TradFi nor DeFi is risk-free. More freedom in DeFi often means greater responsibility in practice.

Conclusion

TradFi and DeFi are better understood as complementary systems, not mutually exclusive teams.

TradFi offers regulated stability, legal recourse, and consumer protections that power real-world finance at scale. DeFi offers openness, programmability, and global access, with transparency and automation baked into the rails.

If you understand how each system works, you can choose the right tool for the job, or combine both with intention.

The details will evolve as regulations and infrastructure mature, but the core mental model will stick: TradFi is institution-led finance, DeFi is software-led finance.

This article is for informational purposes only and does not constitute financial advice. Always do your own research (DYOR) before making any decisions.